Who Are the Winners in the Geosynthetic Industry from the Middle East Conflict?

The Geopolitical Shock to the Global Geosynthetic Polymer Chain

As of April 2026, the escalating conflict in the Middle East has transcended a standard market fluctuation to become a "geopolitical supply shock" that is fundamentally reordering the global petrochemical hierarchy. This is not a temporary disruption; the targeting of energy and chemical infrastructure with missiles and drones has inflicted permanent damage that precludes a return to the "old normal."

The disruption of the Strait of Hormuz—a primary artery for resin exports—coupled with unprecedented polymer price hikes, has created a fractured market where feedstock origin determines survival.

Even if immediate diplomatic breakthroughs occur, future negotiations between Tehran and Washington are unlikely to mitigate the supply shocks, as the destruction of physical infrastructure and the cessation of reliable maritime transit have already decoupled the industry from immediate political outcomes.

We are entering an era where regional availability and feedstock resilience are the only metrics that matter.

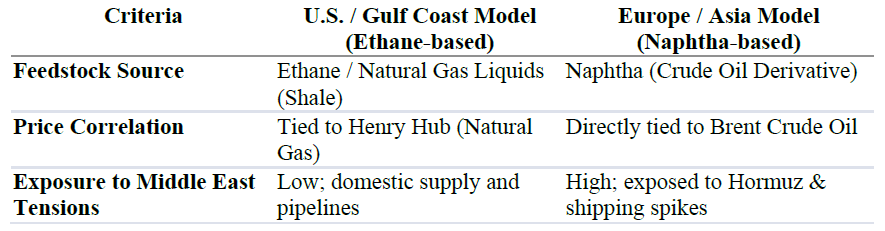

The Feedstock Fault Line: Why the US Shale Advantage is Winning

In the geosynthetics sector, feedstock origin is now the primary determinant of margin resilience. The global industry is bifurcated between the naphtha-based systems of Europe and Asia and the ethane-based systems of the United States. Naphtha, a crude oil derivative, tracks the volatility of Brent crude directly, leading to an "instant cost push" as regional tensions spike. Conversely, U.S. ethane is tied to domestic natural gas markets (Henry Hub), providing a structural buffer against global oil shocks.

The Winners: Dow, LyondellBasell, and Chevron Phillips Chemical

North American giants—specifically Dow Inc., LyondellBasell, and Chevron Phillips Chemical—are the primary beneficiaries of this widening cost gap. While global competitors face margin compression, these U.S. players are seeing significant "margin expansion" by leveraging stable domestic feedstock while selling into a high-priced global market.

Dow, for instance, has implemented aggressive price hikes of approximately 30 cents per pound for HDPE resins in April 2026 alone, following a 10-cent hike in March. This reflects a transition where North America has become the marginal low-cost producer for the world.

Strategic Caveat: The Limits of the Shale Hedge

However, it is important to recognize that the U.S. advantage is relative, not infinite. North American feedstock has a defined ceiling. U.S. fracking firms remain hesitant to invest in new extraction infrastructure despite the crisis, meaning that once current NGL reserves are exhausted, the remaining feedstock could become prohibitively expensive. The U.S. offers a reprieve, not a permanent immunity from global scarcity.

Regional Dominance: The Rise of the Resourceful and the Strategically Stocked

When maritime logistics fail, the depth of strategic reserves becomes the ultimate competitive edge. In this landscape, China has emerged as a dominant winner. While its neighbours face catastrophic disruptions, China’s substantial polyethylene resin reserves and its "coal-tochemicals" infrastructure provide a critical buffer against the Iranian supply shock. Chinese manufacturers like INNO Materials have capitalized on this by maintaining full HDPE resin inventories, allowing them to fulfill orders for both GRI-GM13 and high-performance GM42 geomembranes while other global suppliers declare major supply interruptions.

https://www.inno-materials.com/

The Losers: Regional Attrition and Permanent Closures

The conflict has triggered a sudden drop in global petrochemical operating rates, with the most severe impact felt by:

- Southeast Asian Capacity: Cracker facilities in South Korea, Japan, and Thailand are facing potential permanent closure due to feedstock shortages and uncompetitive naphtha costs.

- Geomembrane Import-Dependent Regions: Australia and New Zealand are particularly vulnerable, facing extreme lead times and insurance premiums.

- Middle East Contract Holders: Geomembrane buyers tied to Gulf-origin contracts face physical supply gaps as cargoes that left before the war's escalation are depleted with no reliable timeline for resumption.

In this environment, availability risk has officially surpassed price risk as the primary concern for project integrity.

Material Innovation and the Substitution Pivot: The NAUE Case Study

As the supply of HDPE geomembranes enters a vacuum, material substitution has evolved from a technical alternative to a critical risk hedge. NAUE has distinguished itself by strategically pivoting to Geosynthetic Clay Liners (GCL) as a substitute for HDPE liners.

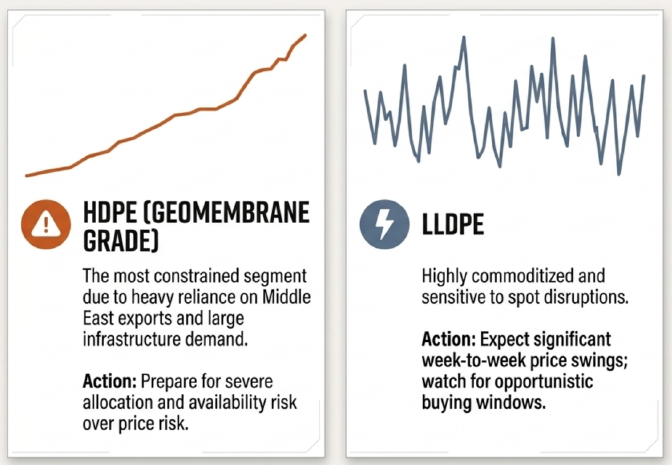

When Supply Chains Fail: Geomembrane Costs are Rising. Lead Times Stretching (ACT NOW!)

In contract negotiations, "substitution rights"—the ability to transition between HDPE, LLDPE geomembranes, or GCL—are no longer optional clauses; they are essential tools for bypassing supply chain bottlenecks. Projects that fail to negotiate technical flexibility into their specifications risk indefinite suspension as HDPE geomembrane lead times continue to stretch.

The Strategic Playbook: Navigating a Persistent Supply Crisis

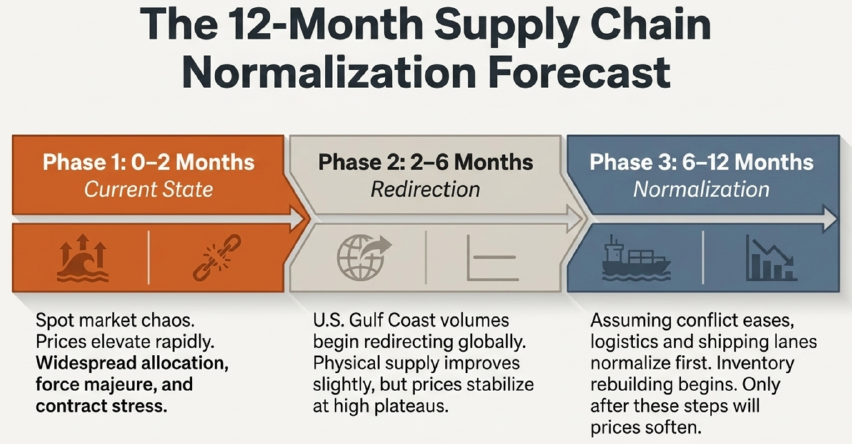

The disruption of Gulf chemical supplies is a multi-year reality. Strategic planning must now be calibrated against a specific temporal roadmap:

- 0–2 Months (The Chaos Phase): Expect continued price escalation, frequent force majeure declarations, and a chaotic spot market. Action: Secure volume now, regardless of current price premiums.

- 2–6 Months (The Redirection Phase): U.S. ethane-based volumes will begin redirecting globally. Action: Shift procurement toward U.S.-origin PE and monitor conversion spreads as resin costs may outpace finished goods pricing.

- 6–12 Months (The New Baseline): Logistics may begin to normalize, but prices will stabilize at a high "new normal." Action: Build a 4–8 week buffer stock to insulate against secondary logistical shocks.

The Bottom Line

The winners of this conflict are those who recognize that the industrial hierarchy has fundamentally shifted. Success belongs to those who secure resin early rather than cheaply, acknowledging that infrastructure damage in the Gulf has rendered the "old normal" obsolete. This is a permanent geopolitical realignment; technical flexibility and feedstock security are now the only viable paths to project completion.